The home of real patriotic British people.

The independent nationalist voice in the UK.

The Red Rose County - Lancashire.

A cummerbund & Griffinite free zone.Nick Griffin wrecked the National Front in the 1980's and then he wrecked the British National Party when he hijacked the BNP in 1999.A blog that supported John Tyndall.

Tuesday, October 04, 2016

Backlash to World Economic Order Clouds Outlook at IMF Talks

‘Creeping protectionism’ poses economic, market risks: fund

World economy likened to driverless car stuck in the slow lane

Policy-making

elites converge on Washington this week for meetings that epitomize a

faith in globalization that’s at odds with the growing backlash against

the inequities it creates.

From Britain’s vote to leave the

European Union to Donald Trump’s championing of “America First,”

pressures are mounting to roll back the economic integration that has

been a hallmark of gatherings of the IMF and World Bank for more than 70

years.

Fed by stagnant wages and diminishing job security, the

populist uprising threatens to depress a world economy that

International Monetary Fund Managing Director Christine Lagarde says is

already “weak and fragile.”

The

calls for less integration and more trade barriers also pose risks for

elevated financial markets that remain susceptible to sudden swings in

investor sentiment, as underscored by recent jitters over

Frankfurt-based Deutsche Bank AG’s financial health.

“The

backlash against globalization is manifesting itself in increased

nationalistic sentiment, against the outside world and in favor of

increasing isolation,” said Louis Kuijs, head of Asia economics at

Oxford Economics in Hong Kong and a former IMF official. “If we lose

consensus on what kind of a world we want to have, the world will

probably be worse off.”

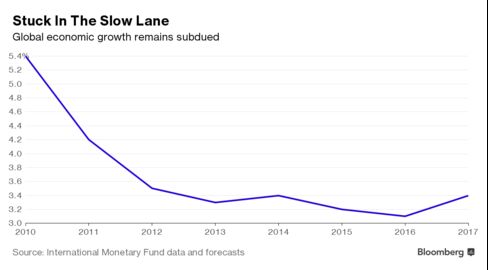

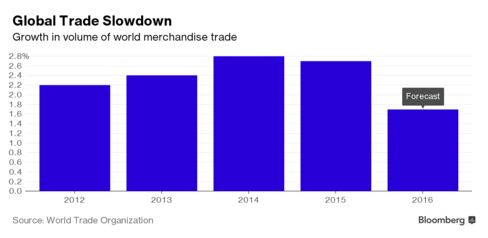

In its latest World Economic Outlook

released Tuesday, the fund highlighted the threats from the anti-trade

movement to an already subdued global expansion. After growth of 3.2

percent in 2015, the world economy’s expansion will slow to 3.1 percent

this year before rebounding to 3.4 percent in 2017, according to the

report, keeping those estimates unchanged from July projections. The

forecasts for U.S. growth were cut to 1.6 percent this year and 2.2

percent in 2017.

“We’d like to see an end to the creeping

protectionism in the world and more progress on moving ahead with

free-trade agreements and other trade-creating measures,” Maurice

Obstfeld, director of the IMF’s research department, said in a Bloomberg

Television interview with Tom Keene.

Lagarde

said last week that policy makers attending the Oct. 7-9 annual meeting

of the IMF and World Bank have two tasks. First, do no harm, which

above all means resisting the temptation to throw up protectionist

barriers to trade. And second, take action to boost lackluster global

growth and make it more inclusive.

Achieving

even those modest objectives may prove elusive. Free trade has become

polling poison in the U.S. presidential campaign, with Democratic

nominee Hillary Clinton now criticizing a trade deal with Pacific

nations, which isn’t yet ratified in the U.S., that she had praised when

it was being negotiated. Republican challenger Trump has lashed out at

Mexico and China, threatening to slap big tariffs on imports from both

nations.Rattled by the U.K.’s June vote to leave the EU, European

leaders know it may just be the start of a political earthquake that’s

threatening the continent’s old certainties. Next year sees elections in

Germany and France, the euro area’s two largest economies, and in the

Netherlands. In all three countries anti-establishment forces are

gaining ground.

Theresa May.

Photographer: Leon Neal/Getty Images

With

growing resentment of the EU from Budapest to Madrid, policy makers

have described the current surge in populism as the greatest threat to

the bloc since its creation out of the ashes of World War II.

Hard Exit

There

are also growing signs that the union and Britain are heading for a

so-called “hard exit” that would sharply reduce the bloc’s trade and

financial ties with the island nation. U.K. Prime Minister Theresa May

said on Oct. 2 that she’ll begin her country’s withdrawal from the EU in

the first quarter of next year.

Perhaps the biggest beneficiary

of free trade over the past generation, China, still restricts access to

many of its key industries, with economists worried about increasingly

mercantilist policies. It’s also seeking a larger role in the existing

global framework, with entry of the yuan into the IMF’s basket of

reserve currencies on Oct. 1 the most recent example.

An all-out

trade war would be a disaster for China’s economy, with Trump’s

threatened tariff potentially wiping off almost 5 percent of its gross

domestic product, according to a calculation by Daiwa Capital Markets.

Waning Support

John

Williamson, whose Washington Consensus of open trade and deregulation

was effectively the governing ethos for the IMF and World Bank for

decades, said the 2008-09 financial meltdown had undercut support for

economic integration.

“There was agreement on globalization before

the crisis and that’s one thing that’s been lost since the financial

crisis,” said Williamson, a former senior fellow at Peterson Institute

for International Economics who is now retired.

The growing opposition to economic integration has been fueled by a sub-par global recovery.

“Perhaps

the most striking macroeconomic fact about advanced economies today is

how anemic demand remains in the face of zero interest rates,” former

IMF chief economist Olivier Blanchard wrote last week in a policy brief

for the Peterson Institute.

The world economy is getting some lift

after rising at an annual rate just shy of 3 percent in the first half

of this year, according to David Hensley, director of global economics

for JPMorgan Chase & Co. in New York.

Driverless Economy

But

much of the boost will come from a lessening of drags rather than from a

big burst of fresh growth, said Peter Hooper, chief economist at

Deutsche Bank Securities Inc. in New York and a former Federal Reserve

official.

Recessions in Brazil and Russia are set to come to an

end, while in the U.S. cutbacks in inventories and in oil and gas

drilling will wane.

“I’m characterizing the global economy as

something akin to a driverless car that’s stuck in the slow lane,” said

David Stockton, a former Fed official and now chief economist at

consultants LH Meyer Inc. “Everybody feels like they’re being taken for a

ride but they’re pretty nervous because they can’t see anybody in

control.”

Upside Risk

Still, for the first time in the

past few years, Stockton said he sees a real upside risk to his forecast

of continued global growth of around 3 percent next year. And that’s

coming from the possibility of looser fiscal policy in the U.S. and

Europe.

In the U.S., both Clinton and Trump have pledged to boost infrastructure spending on roads, bridges and the like.

In

Europe, rising populism provides a powerful incentive for governments

to abandon austerity ahead of the elections next year -- and perhaps

beyond.

Whether such a shift will be enough to mollify those who

have been on the losing side of globalization for decades is debatable,

however.

“The consensus in policy-making circles was that more

trade meant better economic growth,” said Standard Chartered head of

Greater China economic research Ding Shuang, who worked at the IMF from

1997 to 2010. “But the benefits weren’t shared equitably, so now we see a

round of anti-globalization, anti-free trade.

"Globalization will stall for the moment, until we can find a way to share those benefits," he added. http://www.bloomberg.com/news/articles/2016-10-04/existential-threat-to-world-order-confronts-elite-at-imf-meeting

32 comments:

Anonymous

said...

"WE HAVE HEARD THIS BEFORE"

JOBS FOR BRITS British businesses will be ‘named and shamed’ into hiring more UK staff under radical Home Office proposals

Companies will be forced to publish the number of migrants they employ as Amber Rudd attacked the use of cheap foreign labour

FREEDOM IS NOW OFFLINE: Obama Successfully Gives The Internet Away To Multinational Global Entities

US and ICANN officials have said the contract had given Washington a symbolic role as overseer or the internet's "root zone" where new online domains and addresses are created. But critics, including some US lawmakers, argued that this was a "giveaway" by Washington that could allow authoritarian regimes to seize control. A last-ditch effort by critics to block the plan -- a lawsuit filed by four US states -- failed when a Texas federal judge refused to issue an injunction to stop the transition.

Enough! Migrants protest as Switzerland slams border shut in new crackdown SWITZERLAND is the latest country to give up on European cooperation as the government steams ahead with their own plans to clamp down on the migrant influx.

President Hollande has admitted 'France has a problem with Islam' and warned that the country's national symbol will one day be a woman in a burka

Hollande said France 'has a problem with Islam' in a private conversation Said ethnic minority footballers are 'guys from the estates without values' Conversation contained in book called 'A President Should Not Say That…'

Officials are accused of gagging anti-extremism tsar who savages the Government over its failure to manage the impact of mass immigration

Home Office accused of trying to censor Dame Louise Casey's report Study is understood to criticise ministers for failing to integrate minorities and tackle extremism It has been ready for months, according to reports, but publication has been delayed after officials expressed 'unhappiness' about its content

32 comments:

"WE HAVE HEARD THIS BEFORE"

JOBS FOR BRITS British businesses will be ‘named and shamed’ into hiring more UK staff under radical Home Office proposals

Companies will be forced to publish the number of migrants they employ as Amber Rudd attacked the use of cheap foreign labour

https://www.thesun.co.uk/news/1910114/british-businesses-could-be-named-and-shamed-into-hiring-more-uk-staff-under-radical-home-office-proposals/

FREEDOM IS NOW OFFLINE: Obama Successfully Gives The Internet Away To Multinational Global Entities

US and ICANN officials have said the contract had given Washington a symbolic role as overseer or the internet's "root zone" where new online domains and addresses are created. But critics, including some US lawmakers, argued that this was a "giveaway" by Washington that could allow authoritarian regimes to seize control. A last-ditch effort by critics to block the plan -- a lawsuit filed by four US states -- failed when a Texas federal judge refused to issue an injunction to stop the transition.

http://www.nowtheendbegins.com/freedom-now-offline-obama-successfully-gives-internet-away-multinational-global-entities/

PARIS - SEPTEMBER - 2016 (GONE T0 HELL)

https://www.youtube.com/watch?v=ju79YT_lBVI

Actor Says He Impersonated Russian Mercenary in Syria for Sky News Report.

http://www.globalresearch.ca/actor-says-he-impersonated-russian-mercenary-in-syria-for-sky-news-report/5548898

Greek Police Fire Tear Gas at Pensioners Protesting Benefits Cuts

Read more: https://sputniknews.com/europe/20161003/1045944853/greece-tear-gas-pensioners.html

MSM caught misleading readers about Syrian siblings killed in Aleppo

https://www.rt.com/viral/361488-msm-misleading-syria-siblings/

France: The Ticking Time Bomb Of Islamization.

http://www.zerohedge.com/news/2016-10-03/france-ticking-time-bomb-islamization

Cutting immigration matters more to Brits than single market access, poll finds .

https://www.rt.com/uk/361473-britons-single-market-immigration/

Merkel says controversial TTIP deal should STILL go ahead despite wave of European anger

TRADE talks between Europe and the US should continue despite growing opposition from EU member states, according to German leader Angela Merkel.

http://www.express.co.uk/news/world/718116/Angela-Merkel-TTIP-free-trade-deal-negotiations-EU-US-Brussels-Washington

Previously Unseen Footage Catches "Deeply Saddened" Obama Complaining About White Privilege,

http://www.zerohedge.com/news/2016-10-04/previously-unseen-footage-catches-deeply-saddened-obama-complaining-about-white-priv

US seeks to enforce global dominance by unleashing war on countries who oppose it – Assad

https://www.rt.com/news/361623-assad-syria-american-hegemony/

Jew Rabbi Says Jews Working with Moslems to Destroy “Old Europe”

http://www.dailystormer.com/jew-rabbi-says-jews-working-with-moslems-to-destroy-old-europe/

UKIP 'PUNCH' SHOCK Who is Mike Hookem? Ukip MEP ‘who confronted Steven Woolfe in row that turned violent’

Sources say Mike Hookem allegedly 'punched colleague Steven Woolfe' at a party meeting in Strasbourg

https://www.thesun.co.uk/news/1924594/who-is-mike-hookem-ukip-mep-steven-woolfe/

Seems Hookem was 59 Commando/Royal Engineers.

The jewish mixed race chappie Woolfe picked on the wrong one by all accounts.

UKIP Should Be Riding High, but It's Not!

https://www.youtube.com/watch?v=BNBKOORUB5g

Ex British Ambassador Makes Astonishing Speech About Tony Blair, George Bush, War and Profit.

http://truepublica.org.uk/global/ex-british-ambassador-makes-astonishing-speech-about-tony-blair-george-bush-war-and-profit/

Woolfe's got form for being. . . provocative:

https://www.youtube.com/watch?v=VQkbFDtyIIE

"Watch: France's Jean-Marie Le Pen clashes with UKIP MEP Woolfe"

EU, US policies behind crisis behind Syria conflict: France's Le Pen

http://www.presstv.ir/Detail/2016/10/06/487827/syria-france-eu-le-pen

Today’s liberals can be considered mostly as camouflaged communists.

http://visegradpost.com/en/2016/09/02/vaclav-klaus-12-the-eu-is-a-threat-to-europe/

Ex Czech President says EU is a a threat to Europe.

https://twitter.com/HenryMakow/status/784107462735474688/photo/1?ref_src=twsrc%5Etfw

Let’s Make 9/11‘Jewish Remembrance Month!

http://www.realjewnews.com/?p=1153

F**k the Pope.

https://www.youtube.com/watch?v=TXZv9DDCBYw

'Massive evidence foreign-funded White Helmets support terrorist entities in Syria'

https://www.rt.com/op-edge/361957-syria-white-helmets-un/

Refugee centre attacked after wheelchair-bound woman gang-raped in horrific sex assault

FURIOUS protestors launched an attack on a refugee centre after a wheelchair-bound woman was gang-raped by several men.

http://www.express.co.uk/news/world/719661/Refugee-centre-Sweden-attacked-protest-woman-gang-raped-sex-assault

Enough! Migrants protest as Switzerland slams border shut in new crackdown

SWITZERLAND is the latest country to give up on European cooperation as the government steams ahead with their own plans to clamp down on the migrant influx.

http://www.express.co.uk/news/world/712168/Swiss-migrant-crackdown-Italian-border?utm_source=traffic.outbrain&utm_medium=traffic.outbrain&utm_term=traffic.outbrain&utm_content=traffic.outbrain&utm_campaign=traffic.outbrain

President Hollande has admitted 'France has a problem with Islam' and warned that the country's national symbol will one day be a woman in a burka

Hollande said France 'has a problem with Islam' in a private conversation

Said ethnic minority footballers are 'guys from the estates without values'

Conversation contained in book called 'A President Should Not Say That…'

Read more: http://www.dailymail.co.uk/news/article-3834003/President-Hollande-admitted-France-problem-Islam-warned-country-s-national-symbol-one-day-woman-burka.html#ixzz4MskWMvXw

Aggressor squadron? Pics of US jets painted in Russian colors spark Syria false flag conspiracy

https://www.rt.com/viral/362321-us-jets-russian-colors/

Can Jews ever leave their Cult?

http://www.gilad.co.uk/writings/2016/10/12/can-jews-ever-leave-their-cult

What Do Black African 'Refugees' Have To Do With Syria? (Nothing)

http://www.rense.com/general96/blackafrefug.htm

An Act Of Treason – How Bill Clinton Sold Our Missile Targeting Technology To China For Campaign Cash.

http://patriotrising.com/2016/07/12/act-treason-bill-clinton-sold-missile-targeting-technology-china-campaign-cash/

Officials are accused of gagging anti-extremism tsar who savages the Government over its failure to manage the impact of mass immigration

Home Office accused of trying to censor Dame Louise Casey's report

Study is understood to criticise ministers for failing to integrate minorities and tackle extremism

It has been ready for months, according to reports, but publication has been delayed after officials expressed 'unhappiness' about its content

Read more: http://www.dailymail.co.uk/news/article-3829582/Officials-accused-gagging-anti-extremism-tsar-savages-Government-failure-manage-impact-mass-immigration.html#ixzz4My2mInij

Liberal Media Ignore Recent Wikileaks Release "THAT'S CONTROL"

http://dailycaller.com/2016/10/11/liberal-media-basically-refuses-to-cover-recent-wikileaks-release/

Post a Comment